The term Finance Business Partner has suffered from inflation. In too many organisations, it now describes the routine delivery of dashboards, monthly packs, variance commentary and overview slides. The title sounds strategic, but the work often remains trapped in the old finance cycle: collect data, clean data, report data, explain variance, attend a meeting and repeat next month.

A Finance Business Partner should bring something different.

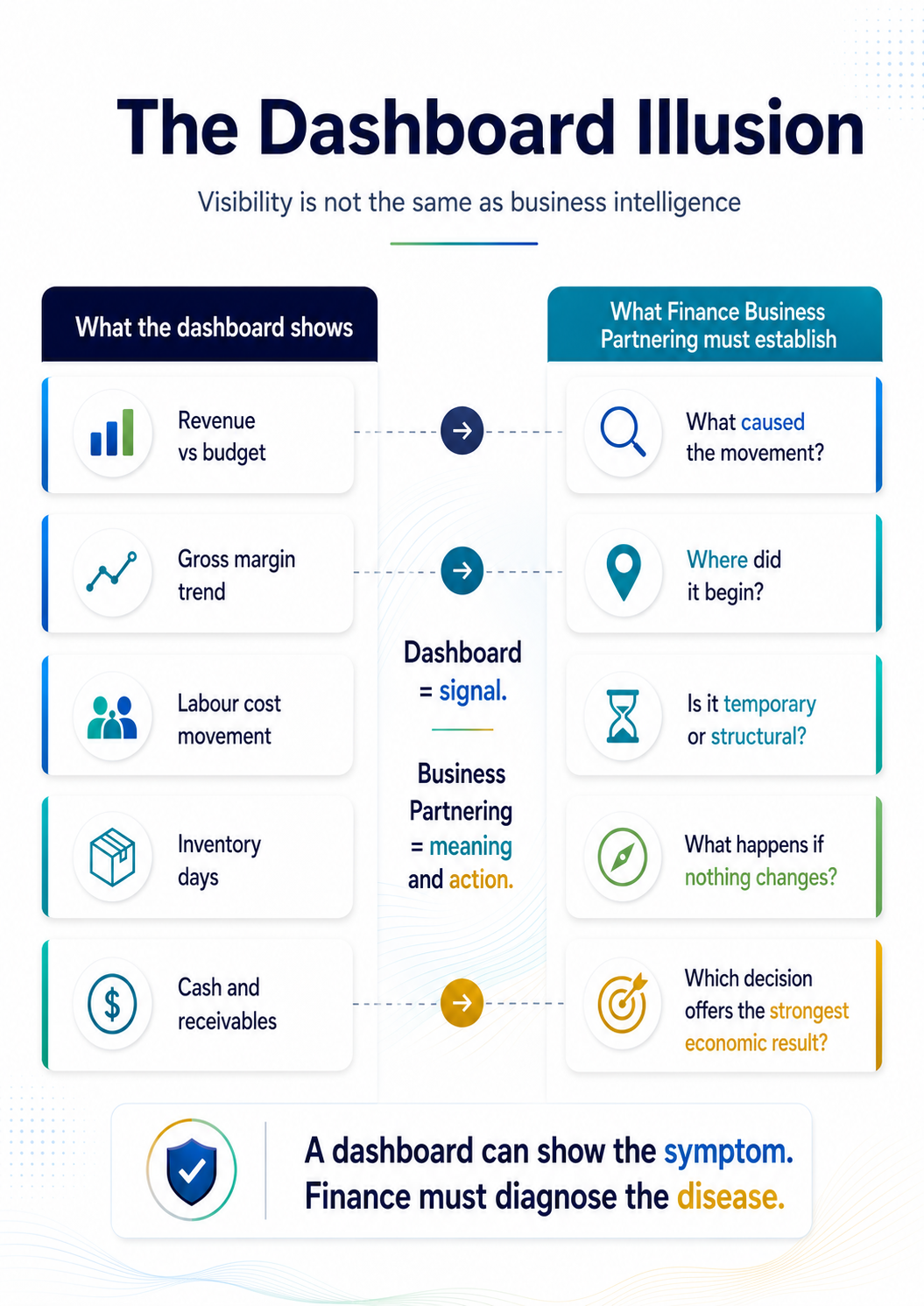

The problem is not the dashboard itself. The problem begins when the dashboard shows a symptom without explaining the business condition behind it. If margin is down by 4.2%, management does not need finance only to confirm that the number is correct. It needs to know why it happened, where it began, whether it is temporary or structural, what will happen if it continues and which realistic response offers the strongest economic result.

Mechanical work should be automated wherever a system can perform it more reliably and economically: data preparation, reconciliation, mapping, standard reporting, variance detection and recurring consolidation. The purpose is not automation for its own sake. It is to release professional capacity for diagnosis, scenario modelling, process improvement, risk interpretation and decision support.

Finance business partnering is therefore not reporting with better language. It is the practical work of connecting numbers to pricing, sales mix, customer behaviour, capacity, labour, inventory, process, margin, cash and risk. It moves backwards from the financial signal to the activity that created it, then forwards into consequences, options and action.

The five-stage test for real finance business partnering

Reporting establishes what happened. Business partnering explains why it happened, what happens next and what management should do.

The dashboard illusion

Dashboards are attractive because they create the appearance of control. Revenue is shown against budget. Gross margin is displayed by month. Labour, cash, receivables, inventory and operational KPIs are presented through charts, indicators and traffic lights. The information may be accurate, visually excellent and available in real time.

But visibility is not the same as business intelligence.

A dashboard can show that gross margin has fallen. It may not establish whether the decline came from discounting, product mix, purchasing inflation, production inefficiency, overtime, rework, waste, customer concentration, incorrect costing or delayed price changes.

It can show that inventory has increased without distinguishing stock that supports planned growth from stock that is slow-moving, duplicated, obsolete or trapped inside an ineffective process. It can show revenue above budget without revealing that the additional sales carry weak contribution, consume excessive working capital or create operational strain.

The dashboard presents movement. The Finance Business Partner must establish meaning.

That is the boundary between reporting and business partnering. Reporting organises information. Business partnering interprets its economic and operational significance and creates a basis for action.

Accurate history is the starting point, not the destination

Historical reporting remains necessary. Accounts must be accurate, reconciliations completed and control maintained. Management needs reliable financial statements and a clear record of performance.

But the work is not finished when the history is correct. Management also needs to know:

- whether the movement is temporary, recurring or structural;

- what caused it and where it originated;

- how quickly it may develop and which areas it may affect;

- what options are realistically available;

- what each option will cost and which risks it introduces;

- and which decision offers the strongest result under realistic conditions.

An adverse labour variance illustrates the difference. The variance may reflect overtime, but overtime may have been caused by weak scheduling, machine downtime, excessive changeovers, absent employees, material shortages or a sales commitment that operations could not fulfil efficiently.

Each cause requires a different response. Recruiting more people will not solve inefficient scheduling. Cutting overtime may damage delivery if the real issue is insufficient capacity. Buying another machine may destroy capital if the existing constraint is poor utilisation rather than inadequate equipment.

Without diagnosis, management can apply the wrong operational treatment to a genuine financial symptom. The report may be correct while the decision based on it is wrong.

Financial analysis is a business diagnosis

Revenue, margin, labour, overhead, working capital, cash, debt and return are not isolated financial categories. They are financial expressions of business activity.

Behind revenue are customers, products, pricing, contracts, demand and delivery capability. Behind gross margin are purchasing terms, labour productivity, material usage, sales mix, discount discipline, waste, rework and costing accuracy. Behind receivables are customer selection, billing processes, disputes, commercial discipline and collection behaviour. Behind inventory are purchasing decisions, supplier reliability, production planning, minimum order quantities, stock controls and operational uncertainty. Behind cash are almost all of them.

The Finance Business Partner therefore cannot remain only inside the general ledger. The ledger records the outcome, but the origin often sits elsewhere: in an incorrectly priced quotation, a sales incentive that rewards revenue without protecting margin, a contract with poor payment terms, weak coordination between sales and operations or a recurring manual error that everyone has learned to tolerate.

Real financial analysis moves backwards from the number into the business activity that produced it. It then moves forwards into the likely consequences and possible decisions.

The “what about it?” test

Every material financial output should survive a simple test:

What should management do because of this knowledge?

If the answer is unclear, the work may still be information rather than insight.

“Revenue is 6% below budget” is information.

“Revenue is 6% below budget because two high-margin product lines are constrained by delayed components while lower-margin sales have grown” is analysis.

“If the constraint continues for another six weeks, the current sales mix will reduce gross profit by approximately £180,000 and create a cash-pressure point in week nine” is forward-looking interpretation.

“Management can protect the result by prioritising available components towards higher-contribution orders, renegotiating selected delivery dates, accelerating an alternative supplier and temporarily limiting low-margin commitments” is decision support.

The difference is not the number of slides. It is the distance travelled from observation to action.

From number to decision

1. Number

The initial signal appears in financial or operational data: margin has fallen, cash conversion has slowed, labour cost has increased, output per hour has declined or inventory days have risen. The number identifies where attention may be required. It does not provide the conclusion.

2. Cause

The next task is to identify the event, process or behaviour responsible for the movement. This may require transaction analysis, customer segmentation, product economics, operational data, process observation, interviews with managers or reconciliation across several systems. One movement can have several interacting causes.

3. Consequence

The cause must then be translated into its wider effect. What will it do to profit, cash, capacity, delivery, borrowing, customer service and risk? A local decision can create consequences elsewhere. Reducing inventory too aggressively may release cash but increase disruption. Extending customer terms may support revenue but weaken liquidity. Cutting maintenance may improve this month’s cost result while increasing future downtime.

4. Opportunity

A problem often contains an opportunity to redesign the activity that produced it. The response may involve pricing, product mix, supplier terms, workflow, capacity allocation, stock policy, contract structure, automation, control or management responsibility. It is often a targeted correction to a recurring activity rather than a large transformation programme.

5. Decision

The final stage is a defined management choice: what will be done, who owns it, when it will happen, what result is expected, which risks are accepted and how progress will be measured. Without this stage, analysis remains an interesting conversation.

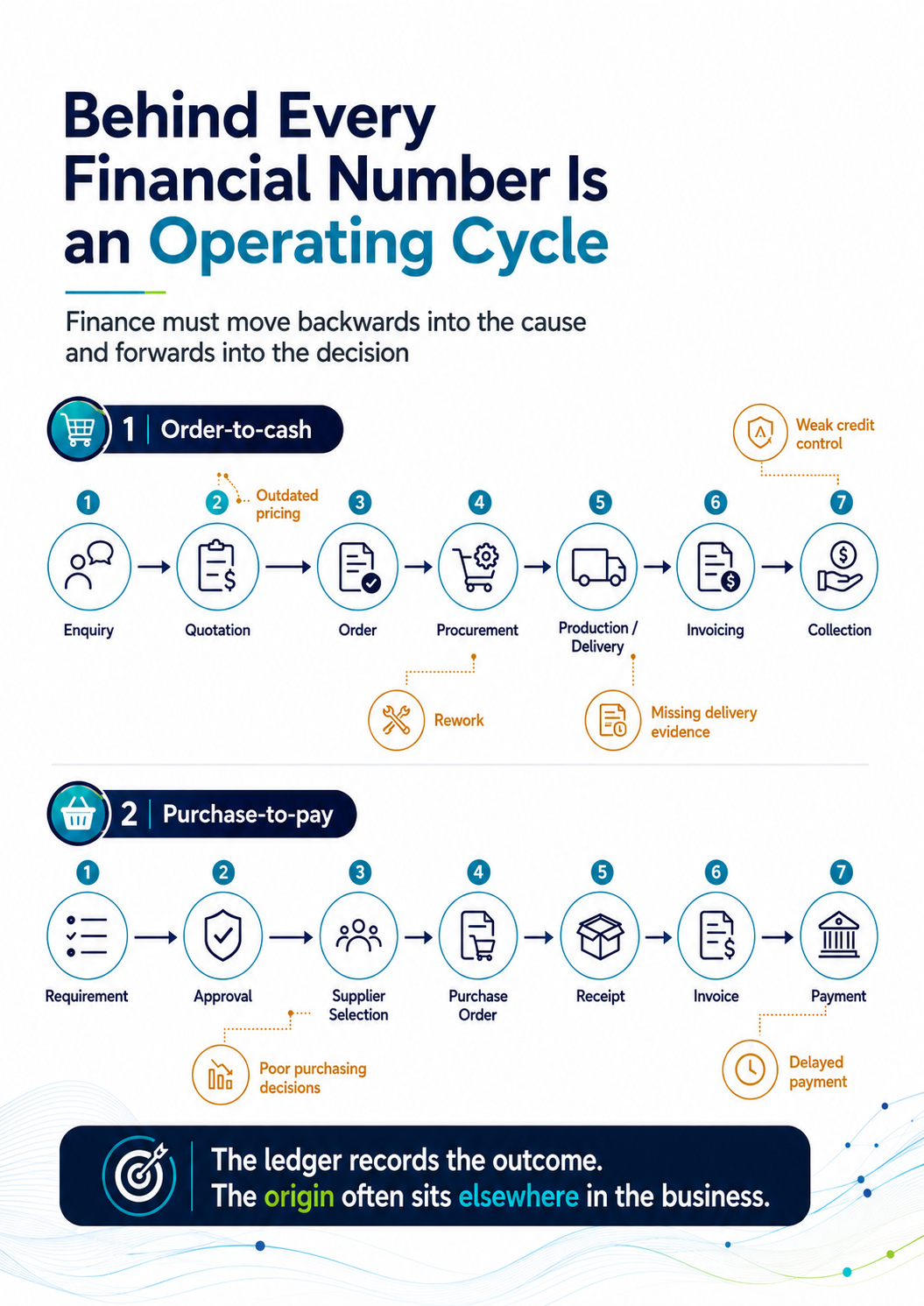

Understand the operating cycle behind the number

Finance business partnering becomes substantially more useful when it understands how the company actually operates. Every organisation has cycles through which value, information, responsibility and cash move.

A typical order-to-cash cycle may run from enquiry to quotation, order, procurement, production or delivery, invoicing and collection. A purchase-to-pay cycle may run from requirement to approval, supplier selection, purchase order, receipt, invoice and payment.

Each stage can introduce delay, error, cost, risk or loss. A quotation may use outdated material prices. An order may bypass credit control. Procurement may optimise unit price while increasing inventory and cash consumption. Rework may never be connected back to the customer or product margin. An invoice may be delayed because completion evidence is missing. A customer dispute may remain invisible until collection fails.

Finance sees the final effect, but the financial effect is often the last stage of a much longer operational story. Understanding that story allows finance to work with the people who own the real cause rather than repeatedly correcting the consequence after it has happened.

When a problem repeats, redesign the process

When the same financial problem appears every month, it is often no longer a reporting problem. It is a process-design problem.

Repeated billing errors, unapproved discounts, late purchase orders, missing delivery evidence, incorrect coding, duplicate data entry, weak stock records and recurring reconciliations consume finance capacity. The traditional response is to add checking, spreadsheets, approvals and people. The process becomes heavier while the error remains.

A stronger response is to redesign the activity so that the error becomes difficult to create. This is the practical principle behind Poka-Yoke, or mistake-proofing: prevent the defect at source rather than relying entirely on later detection.

In finance and operations, this can mean:

- preventing an order below an authorised contribution threshold without approval;

- checking customer credit status before confirming new work;

- requiring delivery evidence before an invoice enters the billing queue;

- validating bank details against approved supplier records;

- preventing duplicate invoices from entering the payment process;

- linking purchasing commitments to cash forecasting;

- and updating product costing when material input prices change significantly.

The objective is not control for its own sake. It is a process that produces more reliable outcomes with less repeated intervention: lower processing cost, fewer errors, faster cycle times, stronger cash conversion and more capacity for valuable work.

Continuous accounting, not monthly reconstruction

Finance often remains trapped in reporting because too much of the month is spent reconstructing the previous month. Data arrives late, reconciliations are delayed, adjustments accumulate and operational information remains disconnected from accounting records. By the time the report is produced, some of the problems have already moved on.

Continuous accounting distributes transactions, reconciliations, accruals, exception handling and operational evidence throughout the period rather than concentrating them into a stressful month-end exercise. This does not remove close control. It applies control earlier and more consistently.

Exceptions can be investigated while the business context is fresh. Missing evidence can be requested before the deadline. Material movements can be examined as they emerge. Forecasts can be updated when conditions change. Month-end becomes confirmation and finalisation rather than financial archaeology.

Faster accounting is not only an efficiency improvement. It increases the period in which management can act. A problem discovered on day three creates more options than the same problem discovered on day fifteen.

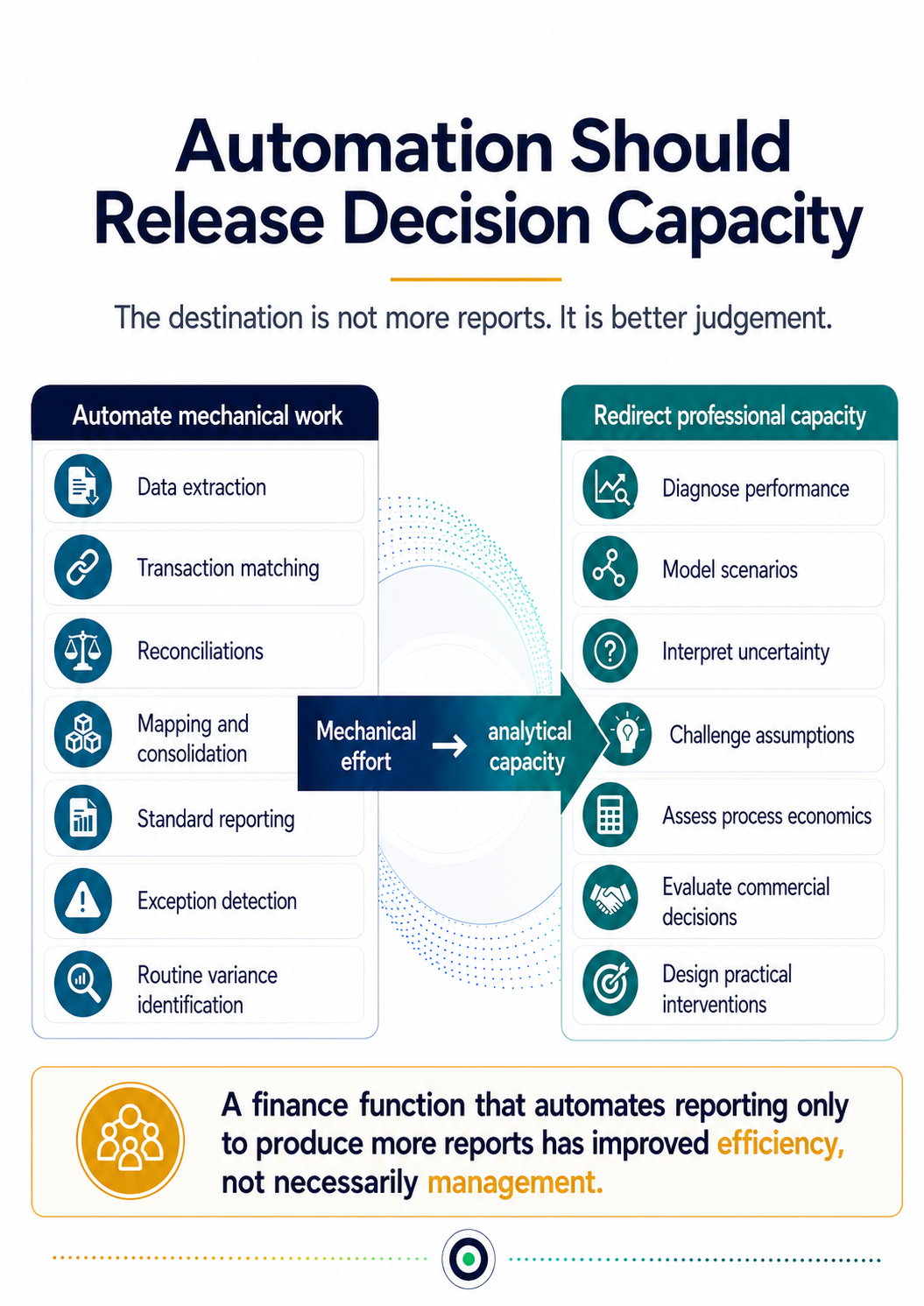

Automation should release decision capacity

Automation supports finance business partnering when it removes mechanical work and releases capacity for diagnosis, scenario modelling and decision support.

Suitable activities include data extraction, transaction matching, recurring journals, reconciliations, mapping, consolidation, standard reporting, exception detection and routine variance identification. But automation is not the destination. A finance function that automates manual reporting only to produce more reports has improved efficiency without necessarily improving management.

Released capacity should move towards work that requires judgement:

- identifying the causes of performance;

- modelling scenarios and sensitivities;

- interpreting uncertainty and challenging assumptions;

- examining process economics and commercial choices;

- assessing operational and financial risk;

- and designing practical interventions.

This is not a crude choice between technology and people. It is a choice between using professional capability for repeated mechanical processing or using it for analysis, judgement and problem-solving. The strongest finance transformation combines reliable systems with people who understand the business and can act on the intelligence those systems produce.

Connected information becomes decision intelligence

Most SMEs already have substantial information across accounting software, CRM, payroll, banking, inventory, project management, e-commerce, production systems and spreadsheets. The problem is often not complete absence of data. It is fragmentation.

Different systems describe different parts of the same event. Definitions are inconsistent, timing differs and ownership is unclear. Management can see many things without understanding what they mean together.

Information becomes valuable when it is converted into context, causality, consequence and choice. A list of overdue customers is information. An analysis showing which customers are slowing, why, which commitments depend on their receipts and which collection actions have the highest probability of success is decision intelligence.

The value is not in possessing more data. It is in improving the decision.

The modern Finance Business Partner

The modern Finance Business Partner is not defined by one report, one system or one meeting. The role combines five forms of contribution.

Interpreter

Connect financial and operational signals to business meaning. Translate the number into the activity, behaviour or process that produced it.

Diagnostician

Separate the visible symptom from the underlying cause. Distinguish an isolated variance from recurring weakness and structural risk.

Challenger

Test commercial and operational assumptions against evidence and economic reality. Challenge should improve the quality of the decision, not create friction for its own sake.

Scenario creator

Model possible futures, trade-offs and consequences under clear assumptions. A scenario does not predict the future with certainty; it makes uncertainty more manageable and prepares proportionate responses.

Decision architect

Structure the path from evidence to action. Compare options, expose trade-offs, clarify ownership, define expected results and establish leading indicators that show whether the intervention is working.

The essential contribution

A Finance Business Partner brings the problem, the diagnosis, the options and the path to a decision.

ERP and BI must move towards possible solutions

Modern ERP and business-intelligence systems are excellent at producing possible data: reports, tables, dimensions, filters, visualisations and transaction-level drill-down. The next stage must focus more strongly on preparing possible solutions.

When a material deviation appears, the system should help establish where it originated, which customers or activities contributed to it, whether it is recurring, what is likely to happen next, which management levers are available and how alternative actions may affect profit, cash and risk.

This does not require technology to make every decision autonomously. It requires technology to prepare a stronger decision environment by connecting evidence, detecting exceptions, identifying patterns and modelling alternatives. Management and finance then apply judgement, commercial knowledge and accountability.

The objective is not a dashboard with more colours. It is a shorter and more reliable distance between a business event and an informed decision.

What this means for SMEs

Large organisations can distribute these responsibilities across FP&A, commercial finance, treasury, risk, process improvement, data engineering and operational-excellence teams. SMEs rarely have that luxury. The same small finance team may be responsible for bookkeeping, compliance, management reporting, cash forecasting, payroll, tax coordination, budgeting, systems and direct support to the owner.

This makes transformation more difficult, but also more important. An SME cannot afford to use scarce professional capacity on work that systems can complete efficiently. It also cannot afford fragmented analysis that identifies problems without creating a response.

SME financial management must connect accounting, cash flow, commercial activity, operations, working capital, process performance, risk and management decisions.

This is the direction behind IBeOne and Horizon Suite: not another collection of disconnected reports, but a decision system that turns financial and operational evidence into practical management intelligence. The purpose is not to overwhelm management with everything the system can calculate. It is to identify what matters, why it matters, what may happen next and what can be done about it.

What management should expect from a Finance Business Partner

For every material deviation, investment question or recurring business problem, management should expect finance to provide:

- the financial or operational signal that requires attention;

- the underlying cause and where it originated;

- the projected consequence if nothing changes;

- the realistic management options and trade-offs;

- the expected profit, cash, capacity and risk effect of each option;

- a clear recommendation under stated assumptions;

- and defined ownership, timing and measures of success.

Not every issue requires a large model or formal project. The standard is proportionality: the quality and cost of the work should correspond to the value and risk of the decision.

Transformation is an operating necessity

Finance transformation is often presented as a large corporate programme, a technology fashion or a presentation topic. For SMEs, it is increasingly an operating necessity.

Margins are under pressure. Customer behaviour changes quickly. Costs move faster. Supply chains remain uncertain. Skilled labour is expensive. Financing is selective. Management must make decisions with limited time and limited analytical capacity.

In that environment, reporting history more efficiently is not enough. Finance must help the company respond. That requires reliable accounting, continuous visibility, connected data, process understanding, forward-looking modelling and clear decision paths.

A Finance Business Partner should be close enough to the business to understand how value is created, rigorous enough to identify where it is being lost and practical enough to help management change the outcome.

The dashboard still has a place. It is the beginning of the conversation, not the final product.

A dashboard can show the symptoms. A Finance Business Partner must diagnose the causes, model the consequences, identify the opportunities and help shape the decision.

That is finance business partnering.

Everything else is reporting with a better title.

Concepts and further reading

- Root-cause analysis and problem-solving methods for separating symptoms from underlying causes.

- Poka-Yoke and mistake-proofing for preventing recurring process defects at source.

- Continuous accounting and continuous close for distributing control throughout the reporting period.

- Scenario planning and sensitivity analysis for evaluating uncertainty, trade-offs and management responses.

- Theory of Constraints and throughput thinking for understanding system-wide rather than local performance.

Explore Horizon Suite

IBeOne is the gateway to Horizon Suite System — built to connect financial evidence, operational conditions, risk and management decisions for SMEs.