A financial forecast can be mathematically correct and still be strategically wrong.

Most forecasts begin with an existing business model. Revenue is projected from current products and customers. Costs are extended from the existing operating structure. Working capital follows established relationships. Investment is assessed through expected savings, additional margin or a defined payback period.

This work is necessary, but it contains an assumption that is rarely stated explicitly: that the economic architecture beneath the forecast will remain broadly valid.

That assumption is becoming less reliable. A company can own profitable assets that are gradually losing strategic relevance. It can reject an apparently expensive capability because its direct three-year return looks weak, only to discover that the same capability later becomes necessary for customer access, process integration or management response. It can improve the margin on one product while becoming increasingly dependent on an external platform that progressively controls its data, access and cost structure.

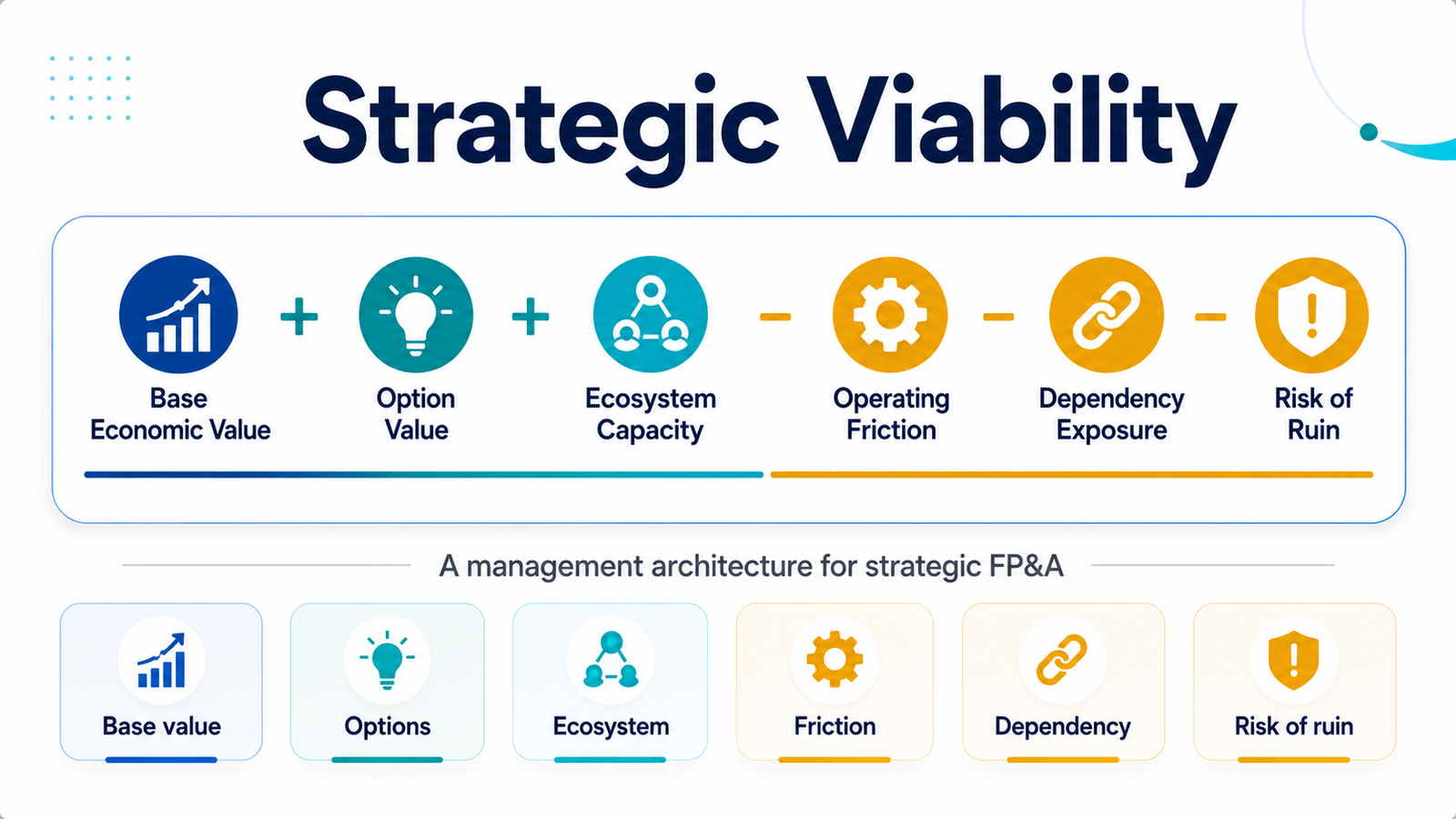

Strategic FP&A must therefore examine more than the expected movement in revenue, cost and cash. It must ask whether the business model remains capable of producing those numbers under changing conditions.

Three structural factors deserve particular attention: the widening gap between recognised accounting value and strategic capability; the growing importance of optimisation and repeatable risk; and the economic power of the ecosystems within which the company operates.

1. The valuation and investment gap

Financial statements remain indispensable. They establish recognised assets and liabilities, measure income and expenditure and provide a controlled account of financial performance. They support stewardship, comparability, compliance and accountability.

But a balance sheet is not intended to be a complete strategic map of every capability the company has created or every opportunity it may eventually monetise.

IAS 38 recognises identifiable intangible assets when the relevant criteria are satisfied. Software, patents, licences, contractual rights and other identifiable non-monetary assets can be recognised in appropriate circumstances. Research expenditure is generally expensed, while qualifying development expenditure may be capitalised only after defined conditions have been met. Internally generated goodwill and many internally developed relationships, brands and organisational capabilities remain outside recognition.

The International Accounting Standards Board began a comprehensive review of IAS 38 in 2024. The project is examining whether the standard remains relevant to current business models and what information investors need about recognised and unrecognised intangibles. The review remained active in May 2026.

What other experts say

Professor Baruch Lev and Feng Gu argue, based on large-sample empirical work, that conventional financial reports have lost part of their relevance to investor decisions as economically important resources have shifted towards innovation, knowledge and other intangible drivers. Their position is deliberately stronger than the argument made here, but it reinforces the need to supplement financial statements with information about the resources and capabilities creating future value.

OECD research reaches a more measured but highly relevant conclusion. Intangible investment has become an important contributor to productivity, but it is harder to finance because its value is uncertain and it offers weaker conventional collateral. This financing constraint is particularly important for smaller and younger businesses that depend on software, organisational knowledge, data, intellectual property and specialised processes.

The practical issue for an SME is therefore not only whether an investment qualifies as an accounting asset. It is whether management can evaluate its economic function adequately.

From static return to strategic investment value

Real-options analysis provides one established way to address this problem. Rather than treating investment as one irreversible decision followed by one forecast, it evaluates the value of managerial choices: the ability to stage, delay, expand, modify or abandon the investment when conditions change.

The work of Avinash Dixit and Robert Pindyck established uncertainty, irreversibility and flexibility as central elements of investment decisions. Uncertainty does not automatically destroy value. Where management retains meaningful choices, uncertainty can increase the value of flexibility.

This is not a proposed accounting standard. It is a management architecture intended to prevent an important capability from being assessed only through its most immediate return.

Capital markets provide visible, although sometimes extreme, illustrations. Alphabet is a mature case: infrastructure, software, technical capability and distribution are reused and monetised across a wide field of customers and applications. SpaceX and OpenAI represent more uncertain valuations in which investors are pricing expectations about infrastructure, reach and future application fields. Whether those expectations justify the price remains an investment judgement.

The lesson for an SME is not to imitate those valuations. It is to distinguish current return from conditional strategic capacity.

Evaluating an integrated planning system

Consider an illustrative 65-employee engineering company evaluating a £180,000 integrated planning and data project. Its conventional three-year business case identifies annual administrative and reporting savings of £55,000, or £165,000 over three years. On that basis, the project does not recover its initial cost and may be rejected.

FP&A then extends the analysis: £70,000 expected working-capital release from faster billing and better inventory visibility; a 40% probability of avoiding a future £100,000 emergency customer-integration project, creating £40,000 of scenario-weighted option value; and £25,000 deducted for implementation contingency, provider dependency and switching preparation.

Against the £180,000 investment, the internal analysis identifies £70,000 of additional modelled economic capacity before discounting for timing. The statutory accounting treatment does not change. The company has simply made a more complete capital-allocation decision.

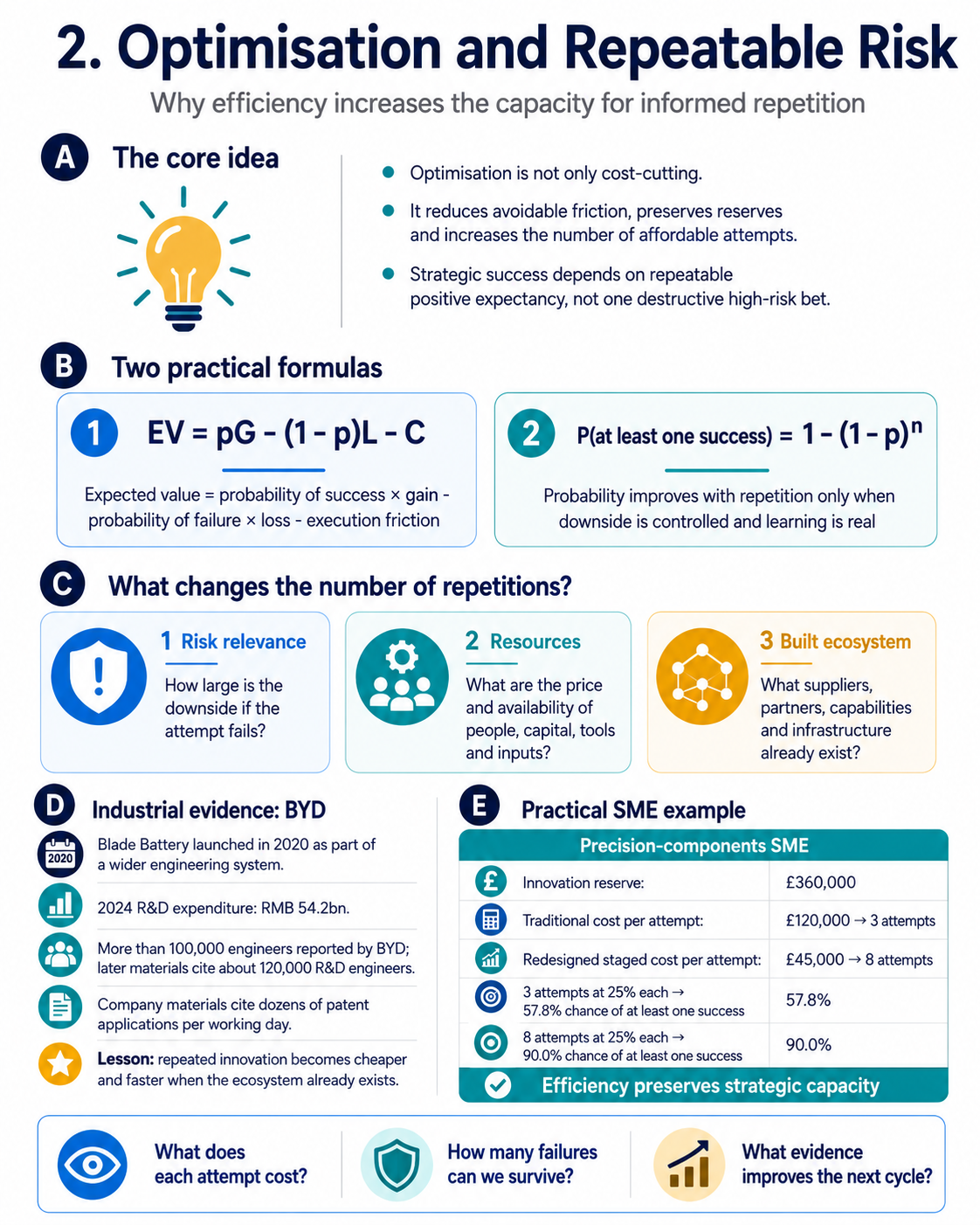

2. Optimisation and the economics of repeatable risk

Competition remains fundamental to business. But the level at which companies compete is changing.

The visible contest may still be between products, prices and brands. Underneath that contest, outcomes are increasingly determined by complete systems: supply chains, access to components and expertise, production scale, information flow, working capital, process reliability, engineering depth and the speed at which learning is converted into action.

Optimisation therefore becomes strategic. It should not be confused with cutting every cost or removing every reserve. An organisation optimised only for current conditions can become efficient and dangerously brittle.

The stronger objective is to remove losses that consume resources without protecting quality, flexibility or resilience. These losses include rework, avoidable inventory, duplicated information, delayed decisions, repeated manual reconciliation, poor-quality customer acquisition and competitive expenditure that creates no reusable advantage.

Reducing those losses does more than improve the current margin. It reduces the cost of each strategic attempt and preserves the resources required to continue.

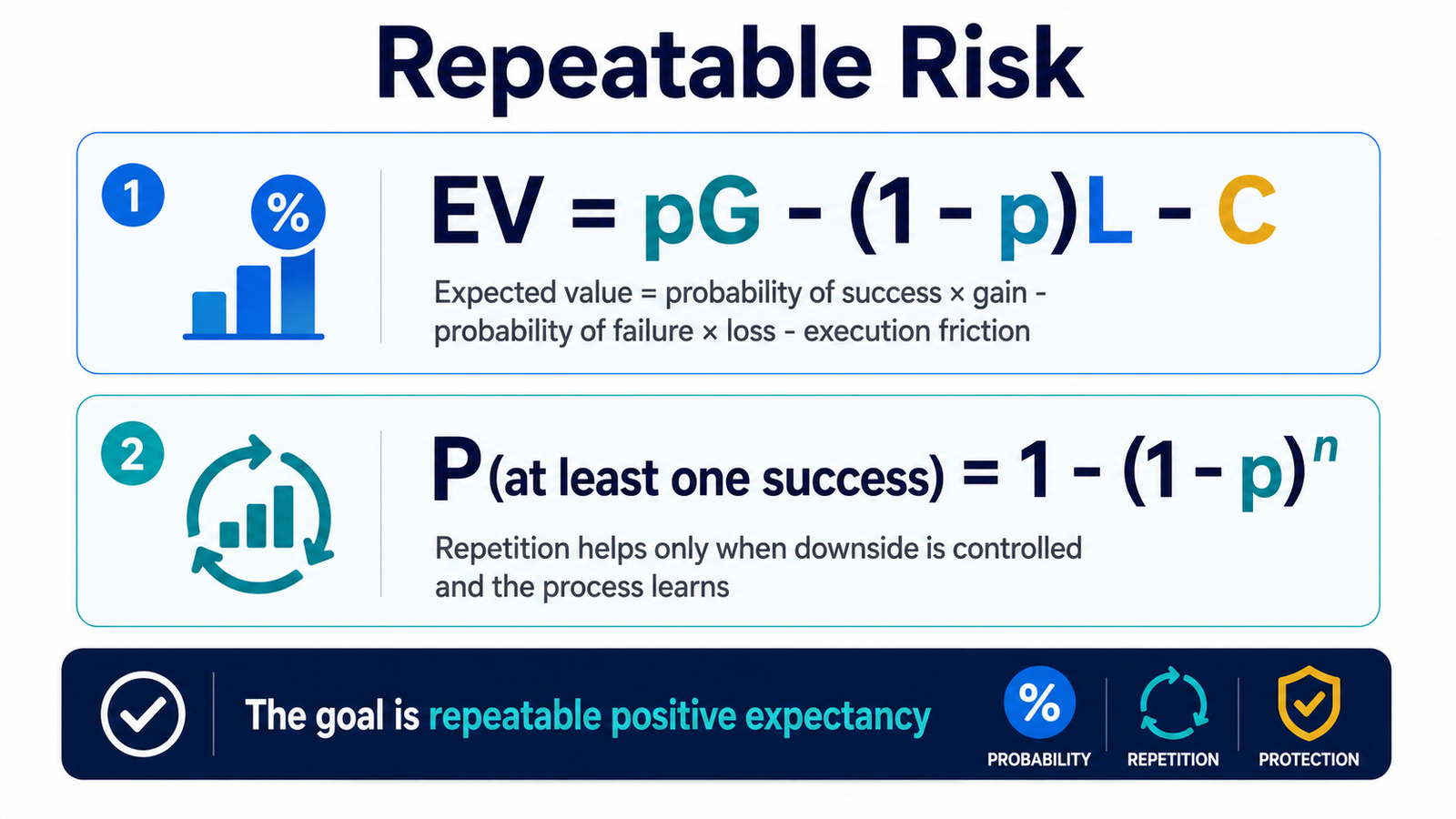

Risk should be designed for repetition

Suppose an initiative has a probability of success, a gain if successful, a loss if unsuccessful and execution friction. The expected value can be represented as:

Repetition does not automatically create success. More repetitions of a negative-expectancy process accelerate destruction. Attempts may also be correlated: the same design error, market assumption or technical constraint may cause several failures. The model is useful only when management controls the downside, preserves sufficient reserves and converts each result into better evidence.

The relevant objective is therefore not maximum risk-taking or maximum risk avoidance. It is repeatable positive expectancy.

What other experts say

Professor Saras Sarasvathy’s research on expert entrepreneurship introduced the principle of affordable loss: under genuine uncertainty, decision-makers frequently begin by defining what they can afford to lose rather than pretending they can predict the complete future return. Her work also stresses the role of committed partners in expanding available resources and reducing uncertainty.

Rita Gunther McGrath and Ian MacMillan’s discovery-driven planning follows a compatible logic. New ventures and uncertain strategic investments should make assumptions visible, test them economically and revise the model as evidence emerges instead of treating the original forecast as a promise.

BYD: innovation capacity as a system

BYD provides a useful industrial illustration. The Blade Battery, introduced in 2020, was not simply an isolated product announcement. It emerged from a company with experience in battery chemistry, manufacturing, vehicle integration, electronics and power management.

BYD reported 2024 R&D expenditure of RMB 54.2 billion, 36% higher than the previous year and greater than its reported net profit. The company stated that annual R&D expenditure exceeded annual net profit in 13 of the 14 years from 2011 to 2024.

Company materials reported more than 100,000 engineers in 2024 and later referred to approximately 120,000 R&D engineers. Patent volume does not prove patent quality, commercial value or technological superiority. It does, however, indicate the scale and repetition capacity of the engineering system.

The company operates inside an even larger industrial structure. In 2025, China accounted for 70% of electric-car production and more than 80% of battery-cell production. Scale, supply-chain structure, manufacturing economics and vertical integration reduce the marginal cost of further attempts.

Measuring whether automation improves the system

During the Industrial Revolution, James Watt gave potential users a comprehensible way to compare the productive power of a steam engine with the familiar work of horses. Modern companies face a related measurement problem when comparing human, technology-assisted and predominantly automated processes.

Daron Acemoglu and Pascual Restrepo’s task-based research distinguishes between automation’s displacement effect and the productivity or new-task effects that may offset it. Moving a task from labour to capital does not automatically mean that the complete system has become more productive.

Goldratt’s Theory of Constraints adds another important qualification. A company does not necessarily improve because every individual activity becomes faster. Overall performance remains governed by the constraint limiting the throughput of the complete system.

Increasing affordable repetitions

Consider an illustrative precision-components SME with a £360,000 innovation reserve. Its traditional route into a new product market requires £120,000 of dedicated tooling and validation for each design. At that cost, its maximum theoretical repetition capacity is three attempts.

Management redesigns the development process. Modular tooling replaces product-specific tooling; a university testing facility is rented rather than built; suppliers provide small pilot batches; digital simulation removes unsuitable designs before physical testing; and each stage requires evidence before the next commitment.

The cost per meaningful attempt falls to £45,000, increasing potential repetition capacity from three to eight attempts. With an illustrative 25% success probability per reasonably independent attempt, the probability of at least one success rises from 57.8% to 90.0%.

Real attempts will not be perfectly independent. The critical benefit is that each cycle should improve the next one. The company has not become less ambitious. It has made its ambition economically survivable.

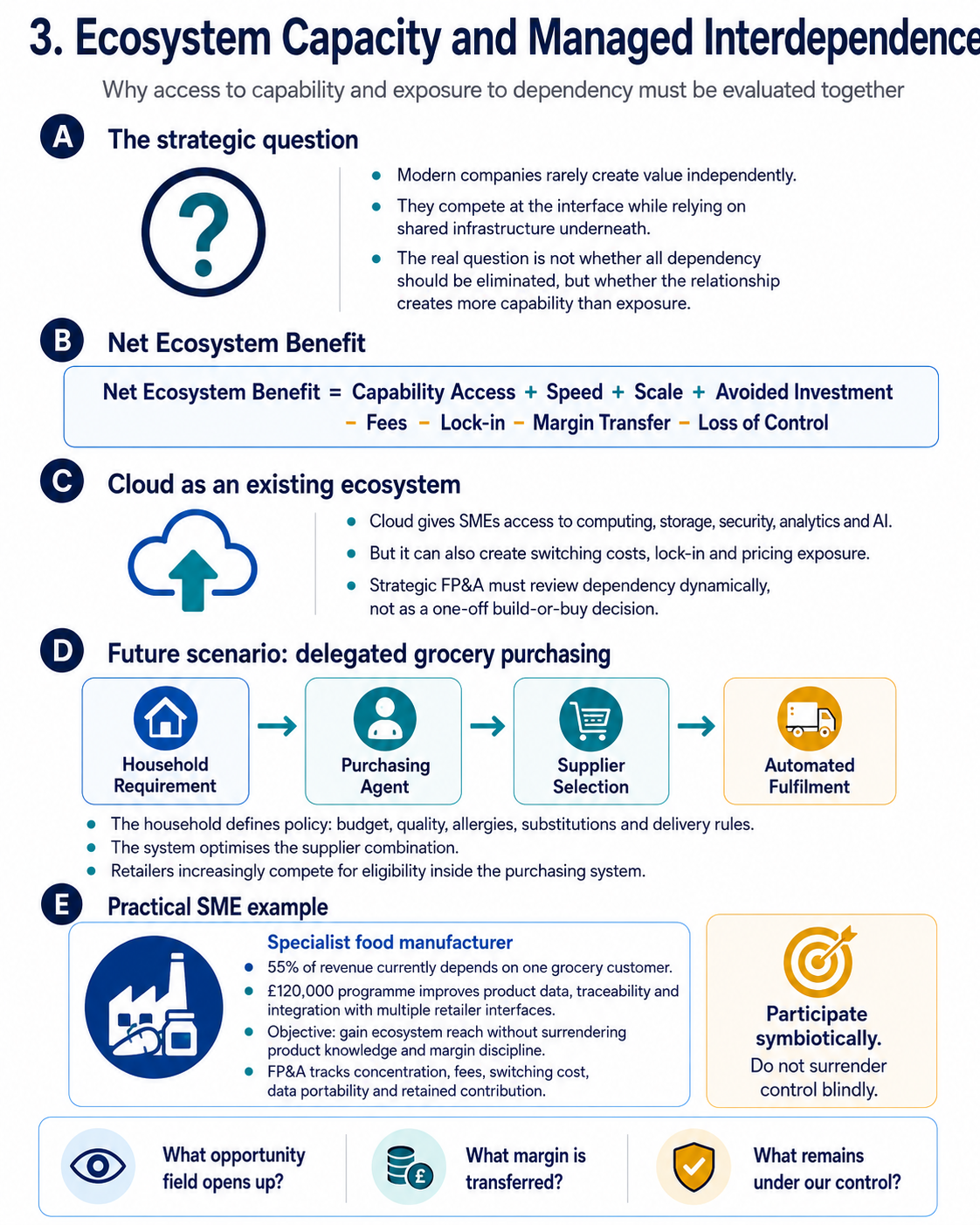

3. Ecosystem capacity and managed interdependence

The modern company rarely creates value independently.

Customers continue to see brands, products and prices competing at the market interface. Underneath that interface, companies increasingly rely on interconnected systems of cloud computing, AI, payments, logistics, manufacturing, data and specialised suppliers.

This creates a layered market. A business can compete through its proposition while cooperating through the infrastructure required to deliver it. It can depend on an ecosystem, contribute value to that ecosystem and compete against other participants operating inside the same structure.

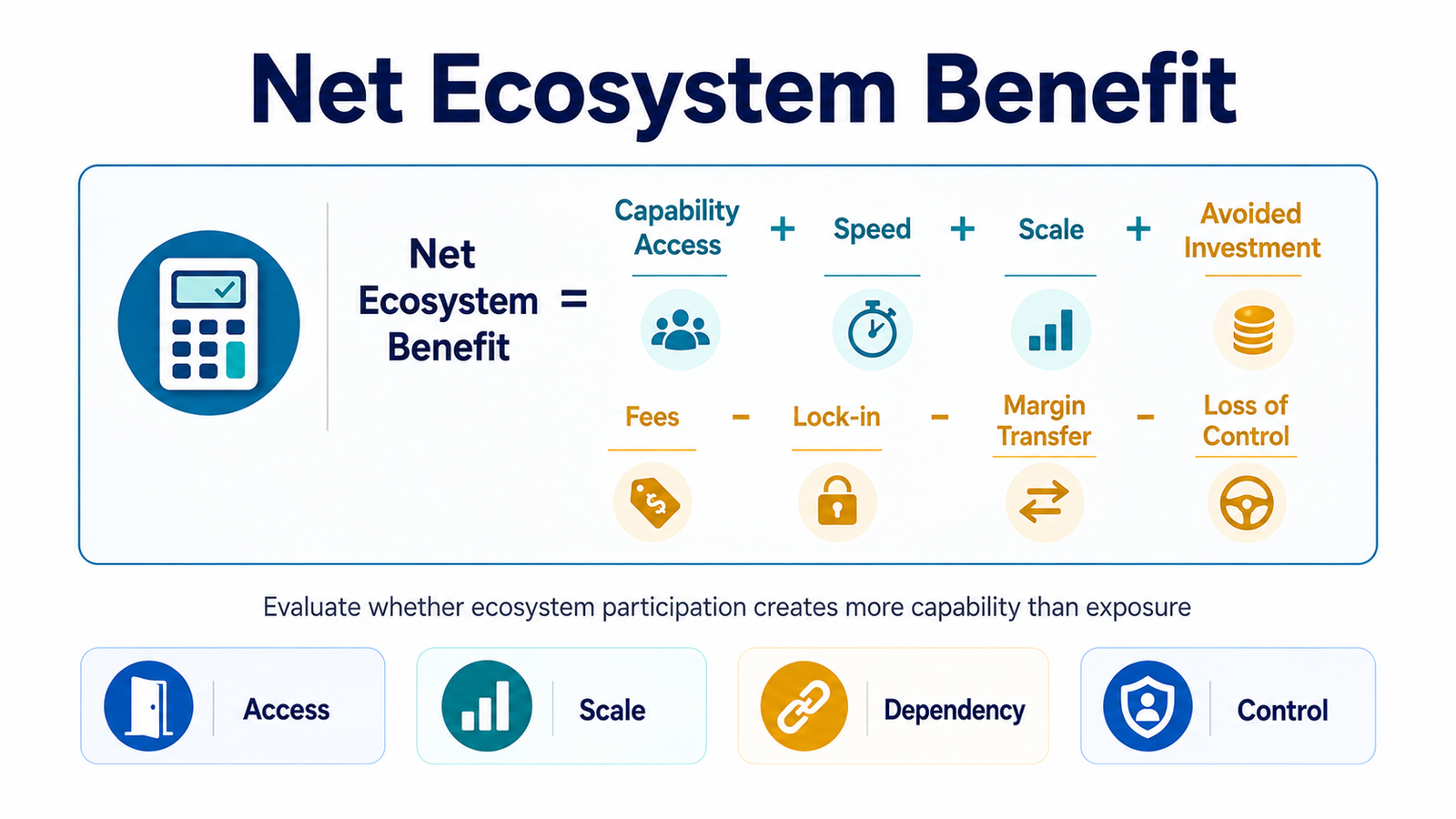

The strategic question is not whether all dependency should be eliminated. It is whether the relationship creates more capability than exposure.

What other experts say

Strategy scholar Ron Adner defines an ecosystem through the alignment of the multiple partners that must interact for a value proposition to materialise. His central point is that excellent execution inside one company may still be insufficient when the result depends on partners, complementors and external infrastructure.

Research by Annabelle Gawer, Michael Cusumano and David Yoffie similarly identifies digital platforms and their associated ecosystems as distinctive structures for creating and capturing value. Platform owners do not merely supply one product. They coordinate access, technical standards and complementary activity across a wider field.

This arrangement creates both opportunity and exposure. Symbiosis must therefore be managed.

Cloud as an existing ecosystem

Cloud infrastructure gives an SME access to computing, storage, security, analytics and AI capability that would usually be impossible to reproduce internally. It reduces the capital and time required to create a new service.

At the same time, it can introduce switching costs, technical lock-in, pricing exposure and dependence on infrastructure controlled by a small number of providers. The UK Competition and Markets Authority’s final cloud-market investigation found that competition was not working well and identified barriers affecting switching, interoperability and customer choice.

A symbiotic strategy does not attempt to defeat the ecosystem provider. Nor does it surrender every distinctive capability to the provider. It decides what should be owned, what may be rented and what alternatives must remain available.

When the customer no longer chooses the store

A future grocery ecosystem provides a practical illustration of how this structure could move into ordinary household consumption.

Imagine a household in which connected appliances monitor routine consumption, the family defines its budget and dietary requirements, and an authorised purchasing agent replenishes what is needed.

The individual components are beginning to emerge. Appliances can recognise and track a limited range of food products. Payment networks are developing infrastructure through which authorised AI agents can discover products, compare offers and initiate transactions under customer controls. Automated grocery fulfilment already combines AI, robotics and high-throughput picking.

The household may define its budget, nutritional and allergy rules, acceptable substitutions, preferred quality, permitted brands, delivery conditions and circumstances requiring direct approval. The system then compares availability, price, full-basket economics and fulfilment performance.

Retailers do not necessarily disappear. Their strategic role changes. They begin competing not only for a customer visit, but also for eligibility inside the household purchasing system.

Participating without surrendering control

Consider an illustrative 40-employee specialist food manufacturer. The company currently earns 55% of its revenue through one grocery customer. It cannot economically build its own national delivery infrastructure, payment network or household purchasing agent.

Management approves a £120,000 programme covering machine-readable product, ingredient and allergen information; real-time stock and batch availability; integration with three retailer or fulfilment interfaces; customer-approved product registration and traceability; and an internal database retaining formulation, margin and customer-use knowledge.

FP&A establishes a position map covering ecosystem-enabled revenue, net contribution after platform and fulfilment fees, revenue concentration by platform, cost and time required to switch, ownership and portability of product data, fulfilment accuracy and internally retained intellectual property.

The strategy is symbiotic rather than confrontational. The SME gains reach, payment capability and fulfilment scale from the ecosystem. The ecosystem gains a differentiated supplier, reliable information and additional transaction volume. FP&A’s role is to ensure that the relationship continues to create more value than dependency.

A broader agenda for strategic FP&A

The three factors now come together.

This is not a universal valuation formula. It is a structure for asking better questions.

On value, FP&A should distinguish direct cash flow from reusable capability and theoretical possibility.

On optimisation, it should measure the cost of failure, the number of affordable repetitions, resource availability, the evidence produced by each attempt and the reserves required to continue.

On ecosystems, it should identify what field of opportunity becomes accessible, what investment is avoided, what margin is transferred, which capabilities remain under internal control, what switching would cost and what happens if access conditions change.

The purpose is not to assign a speculative value to every intangible possibility. It is to prevent management from treating the statutory balance sheet as the whole enterprise, cost reduction as the whole meaning of optimisation or external capability as though it carried no strategic price.

Conclusion

The SME will continue to compete.

But it will increasingly compete through the quality of its investment decisions, the affordability and intelligence of its repetitions and the strength of its position inside wider operating systems.

The economically decisive unit is moving beyond the isolated product. It increasingly includes the system capable of financing, producing, improving, distributing and monetising that product repeatedly.

Strategic FP&A must move with it.

A forecast explains what may happen if the present economic relationships continue.

Strategic FP&A must also ask whether those relationships are the ones on which the company should continue to depend.

Sources and Professional References

- IFRS Foundation — IAS 38 Intangible Assets.

- IASB — Intangible Assets research project.

- Baruch Lev and Feng Gu, The End of Accounting and the Path Forward for Investors and Managers.

- OECD research on productivity, finance and intangible assets.

- Avinash Dixit and Robert Pindyck, Investment Under Uncertainty.

- Saras Sarasvathy — effectuation and affordable loss.

- Rita Gunther McGrath and Ian MacMillan — discovery-driven planning.

- International Energy Agency — Global EV Outlook 2026: Manufacturing and trade.

- BYD company materials and 2024 results concerning R&D, engineering scale and the Blade Battery.

- Daron Acemoglu and Pascual Restrepo — task-based research on automation and labour.

- Eliyahu Goldratt — Theory of Constraints and throughput accounting.

- Ron Adner, “Ecosystem as Structure: An Actionable Construct for Strategy”.

- Annabelle Gawer, Michael Cusumano and David Yoffie — research on platforms and ecosystems.

- UK Competition and Markets Authority — Cloud Services Market Investigation.