For many small and medium-sized businesses, management accounting is still trapped inside the month-end close.

The finance team collects bank statements, card transactions, invoices, supplier bills, payroll reports, expense claims, loan statements, VAT records and spreadsheet schedules. Then it processes accounts receivable and accounts payable, reconciles bank and credit card accounts, posts accruals and prepayments, reviews the Profit and Loss, checks the Balance Sheet, prepares the cash flow statement, builds the reporting pack and finally explains the numbers to management.

All of those tasks are necessary. The problem is not the existence of month-end close. The problem is that, in many SMEs, the close process still depends on manual coordination, spreadsheet stitching, repeated checking and late commentary.

By the time the report is ready, the business has already moved on.

The central question for 2026

Should management accountants continue acting as administrators of accounting data, or should they design finance systems that close faster, detect exceptions earlier and support decisions while there is still time to act?

Professional bodies are already pointing in this direction. ICAEW’s 2026 finance skills outlook highlights strategic acumen, commercial ownership, AI enablement, transformation, credibility and leadership as important finance capabilities for business.[1] AICPA & CIMA research has also shown a clear divide between finance professionals who identify as finance business partners and those who do not, with business-partnering professionals much more optimistic about the future of the profession.[2]

This tells us something important. The future management accountant is not disappearing. But the role is changing.

The 2026 management accountant should not be measured only by how accurately they close the past. They should be measured by how well they build a finance system that helps management see pressure early, understand why it is happening and decide what to do next.

Situation: the month-end close is still too manual

A typical SME month-end close still follows six familiar steps.

- Collect data: bank statements, card transactions, invoices, bills, payroll files, expense reports, credit facilities, loan statements and supporting schedules.

- Process subledgers: AR payments, AP bills, sales invoices, purchase invoices, receipts, supplier payments, credit notes, payroll journals and other movements that need to reach the general ledger.

- Reconcile accounts: bank, card, loan, debtor, creditor, tax, payroll and balance sheet control accounts.

- Post adjusting entries: accruals, prepayments, depreciation, provisions, deferred income, stock adjustments, payroll adjustments and other period-end corrections.

- Review financials: Profit and Loss, Balance Sheet, Cash Flow, working-capital movement, gross margin, overheads and unusual balances.

- Generate reports: management packs, variance commentary, board summaries, cash reports, KPI dashboards and stakeholder updates.

This is normal accounting work. But when these steps are performed mainly through manual extraction, email chasing, uncontrolled Excel files and late reconciliation, the finance team becomes a data-administration department instead of a management-information function.

That is the “Excel Accountant” problem.

Excel itself is not the enemy. Excel remains one of the most useful tools in finance. The real problem is unmanaged Excel: disconnected files, hidden formulas, manual copy-paste routines, no reliable audit trail, no controlled source data and no systematic exception logic.

Recent close benchmarks show why this matters. Ledge’s 2025 month-end close benchmark, based on 100 finance professionals across high-transaction industries, reported that 50% of finance teams take six or more business days to close, and it identifies cash reconciliation as a major bottleneck.[3] Sage’s close-the-books research also positions manual month-end processes as a barrier to faster insight and argues that automation can free more time for strategic work.[4] APQC’s 2025 review of monthly close cycle time makes the same practical point: fewer days spent closing the books means more time available for finance expertise, decision support and higher-value work.[5]

The issue is not that accountants are slow. The issue is that the operating model forces skilled professionals to spend too much time on low-value coordination.

A slow close does not only cost time. It delays visibility. It weakens management response. It turns finance into a historical reporting function when the business needs a decision-support function.

Target: what management accounting should deliver in 2026

Management accounting in 2026 should not be built around a heroic month-end effort. It should be built around a controlled finance architecture.

The target is not blind automation. The target is a controlled, near-touchless close: automated where the rules are clear, human-reviewed where judgement, risk or anomaly exists.

Deloitte describes the financial close as moving from a traditionally manual, time-consuming process toward an automated and continuous cycle. It also notes that leading organisations are adopting near-touchless close processes to improve accuracy, compliance and efficiency while freeing finance teams for value-added analysis and strategic decision-making.[6]

For SMEs, this does not mean every business needs a large enterprise transformation programme. It means the finance function should move towards a practical model where source data is captured consistently, reconciliations run systematically, exceptions are visible early, the reporting pack is generated quickly and the management accountant reviews the business story rather than rebuilding the spreadsheet.

The five questions management accounting must answer

- What happened?

- Why did it happen?

- Is it normal or abnormal?

- What is likely to happen next?

- What should management do now?

This is the difference between reporting history and supporting control.

Architecture: how to achieve an automated month-end close

A practical automated close requires architecture. It is not achieved by buying one AI tool or asking a chatbot to read the ledger. It requires a controlled data and process structure.

The simplest architecture has seven layers.

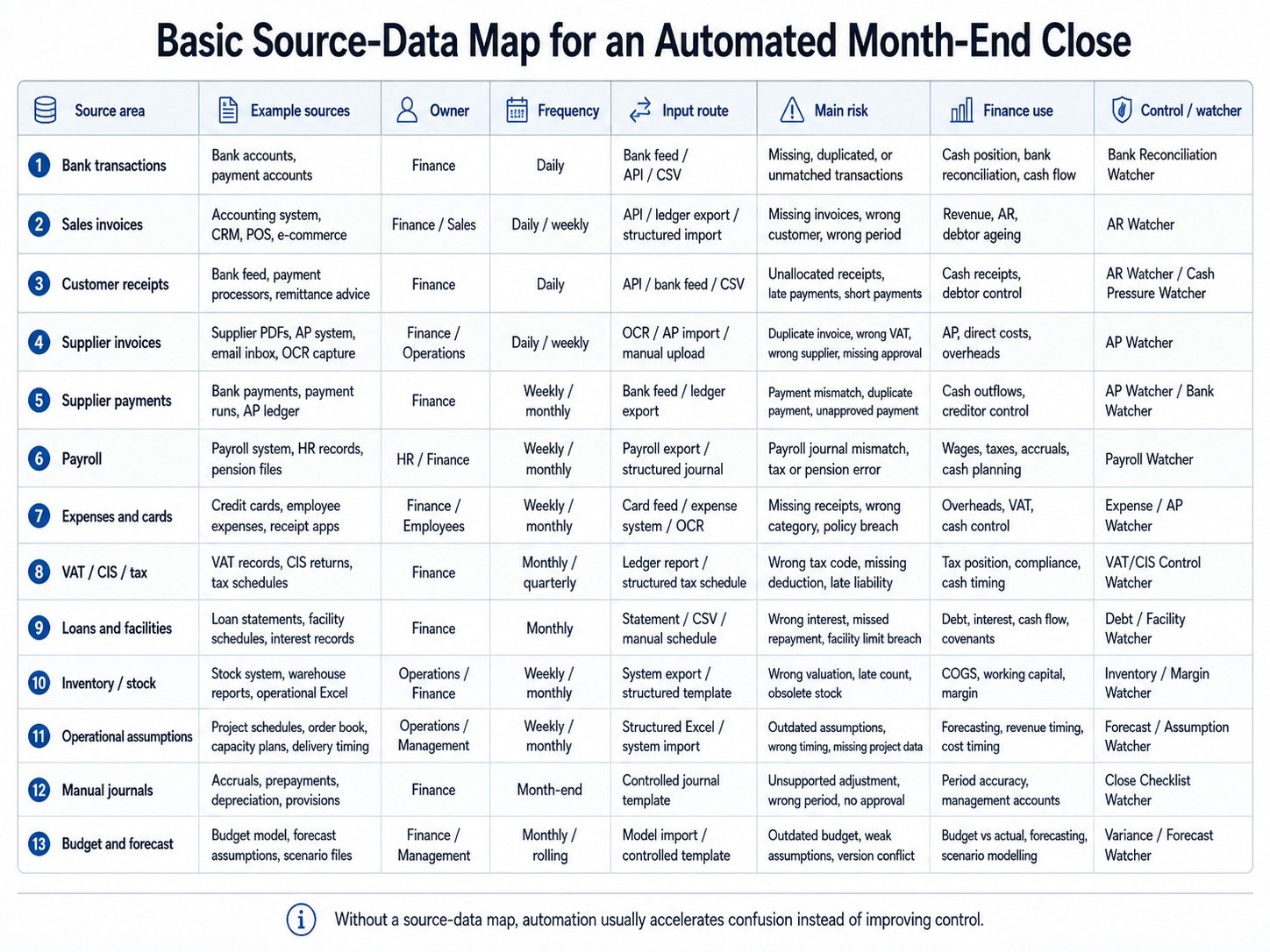

1. Source-data map

The first step is to identify every source that feeds the month-end close.

For an SME, this usually includes the accounting ledger, bank accounts, credit cards, payment processors, sales platforms, CRM, POS or e-commerce systems, payroll, supplier invoices, customer invoices, expense tools, loan and facility statements, VAT and CIS records, stock or inventory data, operational spreadsheets, manual journals and planning assumptions.

Many SMEs discover that the real problem is not accounting skill. The real problem is that data enters the business from too many places without a single controlled route into finance.

Without this map, automation usually accelerates confusion instead of improving control.

2. Controlled ingestion

Once sources are mapped, the business should reduce manual collection.

Data should enter finance through controlled routes: API connections where available, bank feeds, structured CSV imports, standard Excel templates, OCR for supplier invoices and receipts, payroll exports in fixed format, controlled upload areas for operational data, and email or document capture only where properly classified and validated.

The objective is not perfection on day one. The first target is to stop uncontrolled document chasing.

A practical SME can start with five high-value flows: bank transactions, sales invoices and receipts, supplier bills and payments, payroll journals, and VAT/CIS or tax-related data. If these flows are controlled, a large part of the month-end close becomes easier.

3. ETL and standardisation

ETL means extract, transform and load. In plain language, it means taking messy business data and turning it into usable finance data.

This is the layer many SMEs underestimate. They try to automate reports before they have reliable input data. That usually produces faster errors, not better management accounting.

A strong ETL layer should standardise supplier and customer names, map accounts into reporting categories, align dates to the correct period, classify revenue and cost movements, remove duplicates, identify missing fields, validate VAT/CIS coding, match transaction totals back to source totals, preserve data lineage and store rejected rows for review.

Example: a supplier invoice arrives as a PDF. OCR captures supplier, invoice number, date, net amount, VAT amount, gross amount and due date. ETL then checks whether the supplier exists, whether the VAT code is expected, whether the invoice number is already recorded, whether the amount is unusual and whether the expense category matches historical treatment.

If everything is normal, it can move forward. If not, it is flagged. That is the difference between automation and controlled automation.

4. Reconciliation engine

The close cannot be trusted without reconciliation.

The reconciliation engine should compare internal records against external or independent evidence: bank ledger versus bank statement, card ledger versus card statement, AR ledger versus customer receipts, AP ledger versus supplier payments, payroll journal versus payroll report, loan account versus lender statement, VAT/CIS liability versus source transactions and balance sheet control accounts versus supporting schedules.

The point is not that every reconciliation should be fully automatic. The point is that routine matching should be automatic and exceptions should be visible.

| Reconciliation test | Automated logic | Exception flag |

|---|---|---|

| Bank match | Match amount, date, reference and counterparty | No ledger match after tolerance |

| Supplier invoice | Match invoice number, supplier and amount | Duplicate invoice or abnormal amount |

| Payroll | Match payroll report to journal | Net pay, PAYE, NI or pension mismatch |

| Debtors | Match receipt to invoice | Unallocated cash or overdue balance |

| VAT/CIS | Validate tax code and treatment | Code inconsistent with supplier or customer type |

| Loan | Match repayments and interest | Interest accrual not posted |

This turns month-end from manual searching into exception-based review.

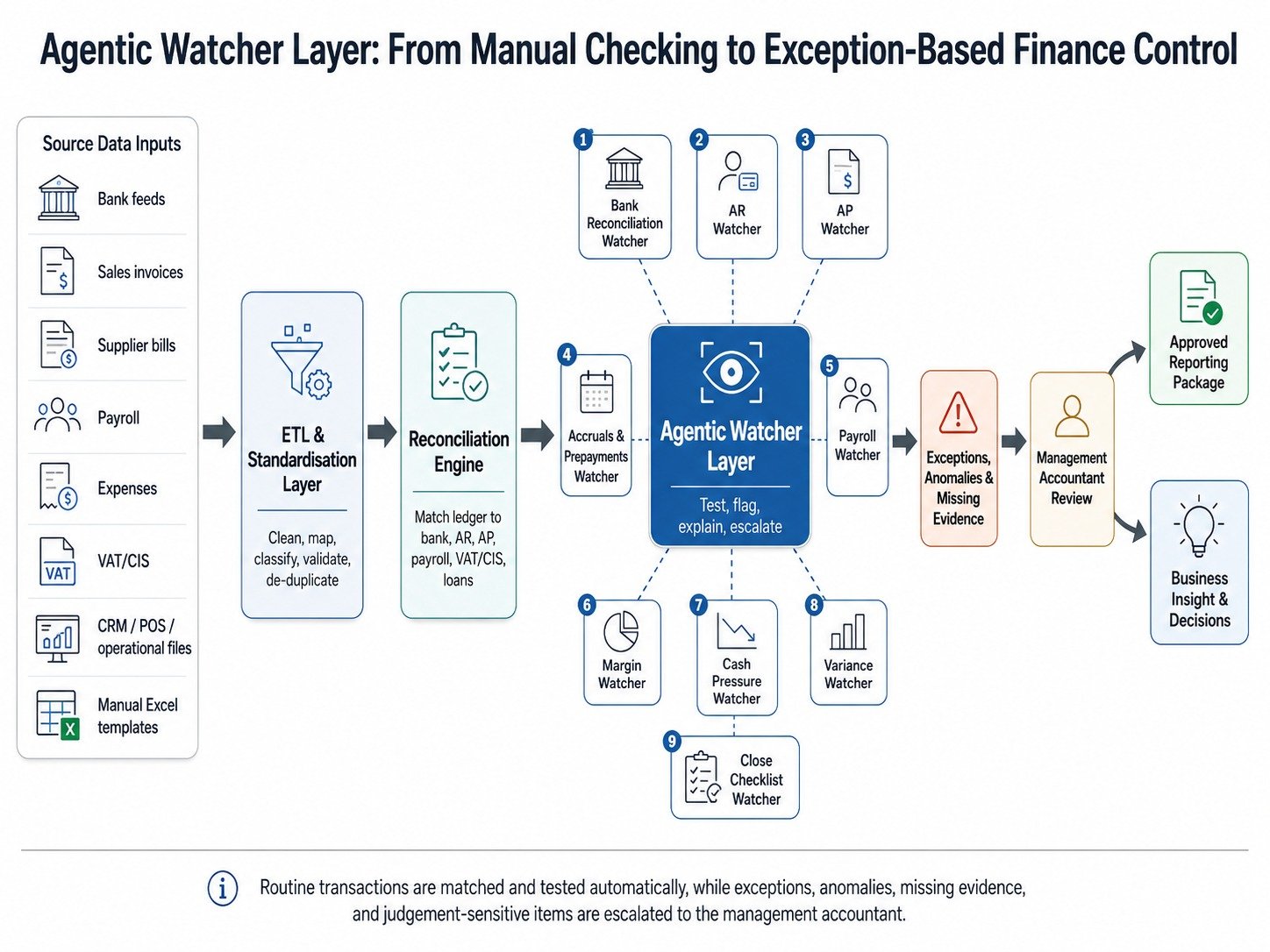

5. Agentic watcher layer

The next step is the agentic structure.

An agentic close does not mean that AI “does the accounts” without control. It means specialised watcher agents monitor defined areas, run tests, identify anomalies and explain what needs review.

Useful watcher agents include bank reconciliation watchers, AR watchers, AP watchers, accruals and prepayments watchers, payroll watchers, margin watchers, cash pressure watchers, variance watchers and close checklist watchers.

The logic is simple:

Match if certain. Flag if uncertain. Explain if abnormal. Escalate if material.

A supplier invoice 3% higher than usual may not matter. A supplier invoice 28% higher than usual, posted to a different cost category, with a new bank account and no purchase approval should be flagged immediately.

A debtor paying three days late may be normal. A debtor whose payment pattern has shifted from 30 days to 58 days should be visible before the cash forecast fails.

A payroll journal that matches payroll reports within tolerance can pass. A payroll journal with unexplained movement in tax, pension or net pay should be reviewed.

This is how AI should support finance: not by replacing professional judgement, but by directing professional judgement to the right place.

There is also a governance reason to be careful. A 2026 accounting reconciliation benchmark, FinBalance, found that contemporary LLMs still struggle with exact balance-sheet accuracy and document-to-ledger consistency in multi-document accounting tasks.[7] That supports a practical conclusion: AI can assist, test, flag, summarise and explain, but finance systems still need deterministic checks, audit trails, reconciliations and human review at material judgement points.

6. Automated reporting package

Once data is ingested, transformed, reconciled and exception-tested, the reporting package should not take days to assemble.

A modern management-accounting pack should be generated from controlled data and include Profit and Loss, Balance Sheet, Cash Flow, 13-week cash flow forecast, revenue analysis, margin analysis, overhead analysis, debtor ageing, creditor ageing, working-capital movement, stock or inventory movement, tax/VAT/CIS position, actual versus budget, current month versus prior month, forecast versus actual, exception list and management action summary.

The management accountant should then work on interpretation.

What changed? Why did it change? Is it temporary or structural? Is cash pressure building? Are margins weakening? Are debtors slowing? Are suppliers stretching? Is stock consuming cash? Are assumptions still valid? What decision is needed?

That is where the value is.

A report that only presents numbers is not enough. A useful management-accounting pack should connect the numbers to action.

7. Close cockpit and control dashboard

The automated close also needs a control layer.

A close cockpit should show close status by task, source data received or not received, reconciliations passed or failed, unresolved exceptions, materiality level, owner responsible, review status, approval status, reporting-pack readiness, post-close corrections and recurring issue trends.

This is important because automation without visibility creates hidden risk.

Management should not be told, “The system closed the month.” Management should be shown what closed automatically, what was reviewed by exception, what remains unresolved, what assumptions were applied, what controls passed and what items need management attention.

That is the standard for a credible automated close.

Result: what changes for the management accountant?

The real benefit of automation is not only speed. The real benefit is role recovery.

The management accountant should not spend most of their professional energy collecting documents, copying data, checking spreadsheets and manually preparing packs.

Those tasks must happen, but they should be systematised.

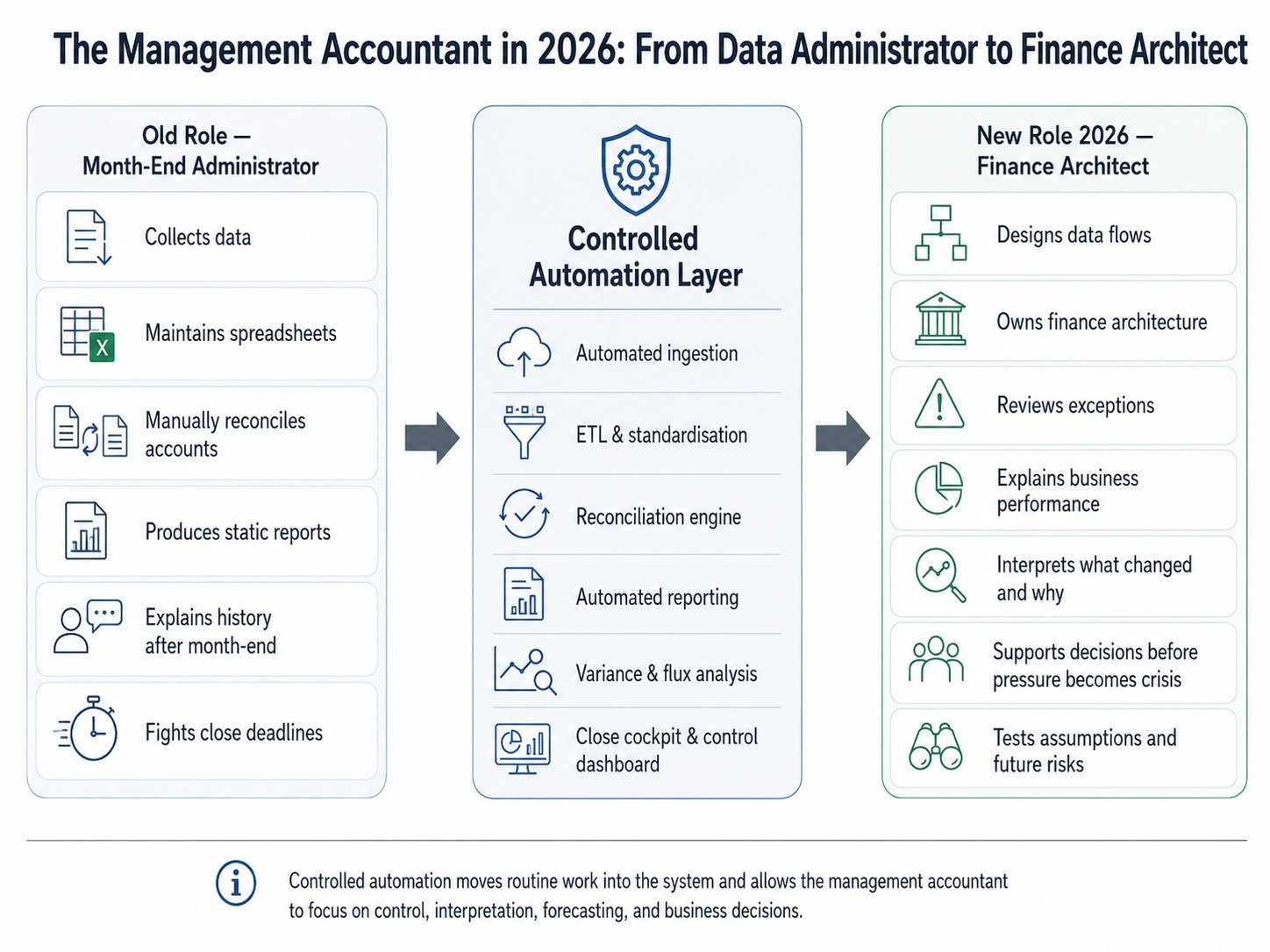

The management accountant’s role should move from data administration to finance architecture and insight.

| Old role | 2026 role |

|---|---|

| Data collector | Data-flow designer |

| Spreadsheet maintainer | Finance architecture owner |

| Reconciliation clerk | Exception-review controller |

| Report producer | Business insight interpreter |

| Month-end firefighter | Early-warning owner |

| Historical commentator | Forward-looking business partner |

| Manual checker | Control-rule designer |

| Budget compiler | Scenario and decision-support modeller |

This is not a reduction in professional value. It is an increase.

The accountant becomes more important because they design the system, challenge the results, interpret the exceptions, explain the business story and support decisions.

ACCA’s AI Monitor describes AI as changing the way accountants work and deliver value, while ACCA commentary on accountant training argues that AI is automating repetitive processes such as data entry and reconciliation, freeing accountants to develop analytical and advisory skills earlier.[8] Gartner has also predicted that by 2026, 90% of finance functions will deploy at least one AI-enabled technology solution, while fewer than 10% will see headcount reductions as a result.[9] The implication is clear: the direction is not simply job replacement. It is work redesign.

Practical application: what an SME can do first

A small or medium-sized business does not need to implement everything at once.

A practical roadmap can start with five steps.

Step 1: measure the current close

Before automation, measure the baseline: how many working days the close takes, how many people are involved, how many Excel files are used, how many source systems are manually exported, how many reconciliations are manual, how many post-close corrections happen, which tasks create delay, which data sources are least reliable and which reports are produced but not used by management.

Step 2: build a close checklist

A close checklist should define the task, owner, source data, due date, dependency, control test, evidence required, review status and approval status. A close process that exists only inside people’s heads cannot be automated properly.

Step 3: automate the highest-friction data flows

Start with the flows that cause the most delay: bank transactions, supplier invoices, sales invoices, payroll, VAT/CIS, expense claims, debtor receipts and loan statements. The objective is not to automate everything at once. The objective is to remove repeated manual collection and reduce data-entry risk.

Step 4: create exception rules

Create rules such as: flag bank transactions with no ledger match after three working days; flag supplier invoices above historical tolerance; flag duplicate invoice numbers; flag customer balances older than agreed terms; flag payroll movements above expected variance; flag VAT/CIS treatment outside expected supplier or customer profile; flag gross margin movement above tolerance; flag negative cash weeks in the 13-week forecast; and flag balance sheet accounts without supporting schedules.

Step 5: generate the reporting pack automatically

Once the data and controls are reliable, the reporting pack should be generated from the system, not rebuilt manually. This is where the management accountant returns to proper professional work: variance analysis, root-cause explanation, cash interpretation, margin review, working-capital control and management action.

Example: a practical automated close flow

Imagine an SME with sales invoices, supplier bills, payroll, bank feeds, VAT/CIS obligations and a rolling cash forecast.

At the end of the month, the system should already know which invoices were issued, which customers paid, which debtors are overdue, which supplier bills were received, which payments were made, which payroll journals were posted, which bank transactions are unmatched, which VAT/CIS positions are building, which accruals may be needed, which prepayments should be spread, which balances changed abnormally and which weeks in the next 13 weeks show cash pressure.

The accountant should not discover these things after several days of manual checking.

The system should flag them continuously.

By the time the month closes, most routine matching, classification and validation should already be done. The remaining work should be exception review, judgement, final approval and explanation.

This is how a close that once took days can move towards minutes for reporting-package generation after data validation and exception clearance.

The 13-week cash flow as the management navigation layer

The month-end close should not finish with static reports only.

For SMEs, the 13-week cash flow forecast is one of the most practical management tools because it connects accounting to operational reality.

A Profit and Loss account may show profit while cash pressure is building. A Balance Sheet may show receivables while customers are paying late. Sales may look strong while supplier payments, payroll, tax, loan repayments and stock purchases collide in the same future week.

The 13-week forecast forces the business to answer: when will cash actually arrive, when must cash leave, which debtors are critical, which supplier payments are unavoidable, where are payroll, VAT, CIS, rent, loans and facilities due, what is the minimum cash buffer, which week creates the greatest pressure and what decision is needed before that pressure arrives?

This is where management accounting becomes live decision support.

The close tells management where the business stands. The 13-week forecast tells management where the business is going next. Both must be connected.

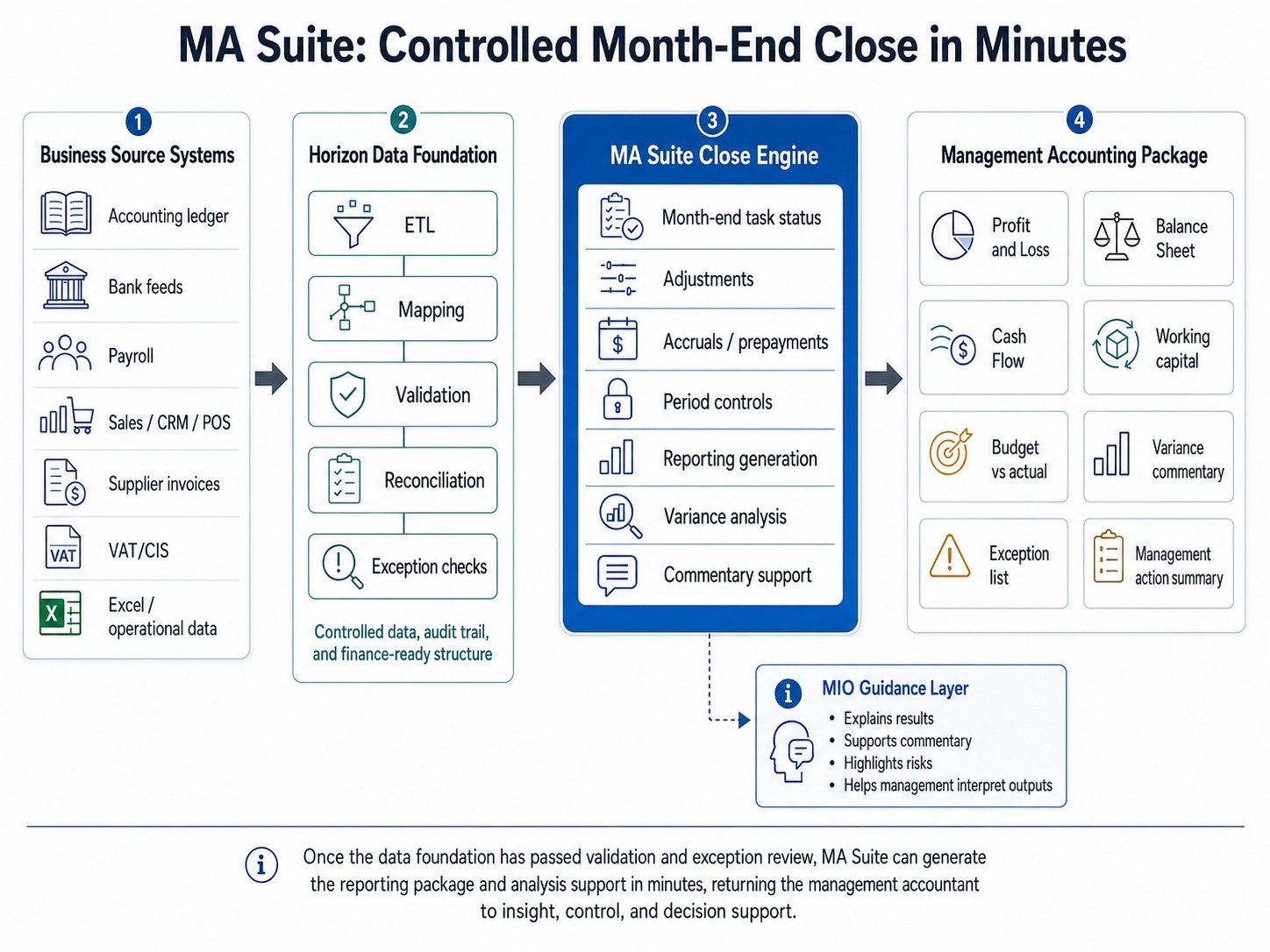

Where Horizon Suite and MA Suite fit

This thinking is central to Horizon Suite.

One of the submodules, MA Suite, is designed around the principle that the month-end reporting package should not require days of manual reconstruction once the data foundation is connected, validated and reconciled.

The goal of MA Suite is to support a controlled close where management-accounting outputs, reporting packages, variance analysis and analytical support can be produced in minutes after the required data has passed validation and exception review.

The purpose is not to replace the management accountant.

The purpose is to remove the administrative drag that prevents proper management accounting.

In this model, the system supports structured data ingestion, ETL and mapping, reconciliation checks, exception flagging, automated reporting, variance detection, management commentary support, connection to cash-flow visibility and decision-focused analysis.

The accountant remains responsible for professional judgement, interpretation, challenge, approval and business advice.

That distinction matters.

Automation should not create a black box. It should create a controlled finance environment where the accountant can see the source, the rule, the exception, the adjustment, the report and the management implication.

Review and control: how to test whether the system works

A modern close is not successful only because it is fast.

It is successful because it is fast, controlled, explainable and useful for decisions.

| Control area | Measurement |

|---|---|

| Close speed | Hours or days from period end to reporting pack |

| Automation coverage | Percentage of close tasks automated or semi-automated |

| Data quality | Number of missing, duplicated, rejected or corrected records |

| Reconciliation quality | Unmatched items by count and value |

| Exception volume | Number of unresolved exceptions at close |

| Manual journal dependency | Manual journals as percentage of total journals |

| Post-close correction rate | Adjustments required after reporting-pack release |

| Reporting usefulness | Number of management decisions supported by the pack |

| Forecast accuracy | Projected versus actual cash variance |

| Working-capital visibility | Debtor, creditor, stock and cash pressure detected before close |

| Audit trail | Ability to trace source, transformation, rule, exception, review and approval |

This is where many automation projects fail. They measure whether the software runs. They do not measure whether the finance function has become more useful.

The test should be simple: can we close faster, explain more clearly, detect risk earlier, reduce manual correction and help management act sooner?

If the answer is yes, automation is working.

If the answer is no, the business has only digitised the old pain.

The real meaning of management accounting in 2026

Management accounting in 2026 should not be a monthly reporting ritual.

It should be a control and insight system.

It should connect data, accounting, cash, working capital, margin, forecasting and management decisions.

The best management accountants will not be the people who work hardest at month-end. They will be the people who design finance systems that make month-end less painful, more controlled and more useful.

The future of management accounting is not a faster spreadsheet.

It is a controlled finance architecture where routine close work is automated, exceptions are flagged, reports are generated quickly and the accountant’s time is redirected toward insight, control, forecasting and decision support.

The management accountant should not be reduced to an administrator of accounting data.

The management accountant should become the person who helps the business understand what happened, why it happened, what is likely to happen next and what management should do about it.

That is what management accounting should look like in 2026.

Notes and Source Basis

- ICAEW, Seven in-demand finance skills and roles for businesses in 2026, and related ICAEW 2026 skills commentary on accounting roles including storytelling, cloud specialism and systems integration. Source.

- AICPA & CIMA, New AICPA and CIMA research shows deep divide among finance professionals, used to support the shift toward finance business partnering and changed expectations of finance roles. Source.

- Ledge, Month-End Close Benchmarks for 2025, used as practitioner evidence for close duration, Excel dependence and reconciliation bottlenecks. Source.

- Sage, Close the Books research and close-automation commentary, used as practitioner evidence for manual close burden and the value of automation in freeing finance time. Source.

- APQC, Cycle Time to Perform Monthly Close, used to support the practical argument that close-cycle reduction frees time for decision support and higher-value work. Source.

- Deloitte, Controllership and Financial Close, used to support the move from manual close to automated, continuous and near-touchless close models. Source.

- FinBalance academic benchmark on accounting reconciliation and LLM limitations, used to support the governance argument that AI outputs still require deterministic checks, reconciliations and human review. Source.

- ACCA, AI Monitor, and related ACCA commentary on AI changing accounting work, used to support the argument that repetitive processing can contract while advisory and analytical work expands. Source.

- Gartner press release predicting AI-enabled technology adoption across finance functions by 2026, used to support the direction of finance work redesign. Source.

Source List

- ACCA — AI Monitor.

- AICPA & CIMA — Finance professional research and future-of-finance commentary.

- APQC — Monthly close cycle-time analysis.

- Deloitte — Controllership and Financial Close.

- FinBalance / arXiv — Accounting reconciliation benchmark for LLM limitations.

- Gartner — Finance-function AI adoption prediction.

- ICAEW — 2026 finance and accounting skills outlook.

- Ledge — Month-End Close Benchmarks 2025.

- Sage — Close the Books research and automation commentary.